The Situation

Food Co.* had long emphasized profits at the expense of brand equity, product innovation, market leadership and category strategy. The company returned to growth mode by getting back to basics: focusing on its core, promoting hero brands and eliminating weak sellers.

Our Approach

- A renewed focus on core and hero brands.

- Coordinated plans for hero brands. We worked with cross-functional teams—notably sales and marketing leaders—to redirect media spending to hero brands, rationalize SKUs and outline promotion and pricing strategies.

- New retail partnerships to reclaim category leadership.

- New brand launch to reach a high-potential customer segment.

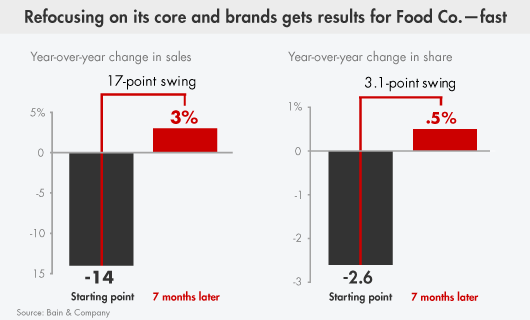

The Results

* We take our clients' confidentiality seriously. While we've changed their names, the results are real.